The debt collection process plays a crucial role in maintaining financial stability, both for creditors seeking repayment and borrowers striving to resolve their obligations. It is more than just a series of actions; it represents the balance between financial accountability and consumer rights.

Understanding the stages of debt collection and the rights involved is essential for navigating this complex process. From early missed payments to legal actions, each step carries specific implications for both parties. Awareness of these rights empowers individuals to handle their debts effectively while ensuring creditors operate within legal boundaries.

This article will delve into the stages of the debt collection process, outline the rights and responsibilities of all parties, and provide practical insights into managing debt and avoiding common pitfalls. By the end, you’ll gain a comprehensive understanding of how debt collection works and how to approach it proactively.

The Role of Debt Collection in Financial Management

Debt collection serves as a cornerstone for maintaining healthy financial relationships between lenders and borrowers. It ensures that both parties operate within a framework of trust and clarity, fostering an environment where financial obligations are met in a timely and efficient manner.

1. How Debt Collection Helps Maintain Lender-Borrower Relationships

Building Trust and Clarity: A structured debt collection process provides transparency for both creditors and debtors, clearly outlining repayment obligations and expectations. This clarity strengthens the trust needed for sustainable financial partnerships.

Encouraging Timely Payments: By addressing missed payments promptly and professionally, debt collection reduces the likelihood of defaults, helping borrowers stay on track and lenders recover their funds without delays.

2. The Impact of Effective Debt Collection on Financial Stability

Reducing Financial Risks for Lenders: A well-implemented debt collection strategy mitigates financial losses by ensuring that unpaid debts are pursued systematically. This stability allows lenders to maintain liquidity and offer credit to new customers.

Helping Borrowers Manage Repayment Obligations: Debt collection, when handled ethically, aids borrowers in understanding their financial responsibilities and finding manageable repayment solutions. This balance promotes financial stability on both ends of the transaction.

By bridging the gap between financial accountability and support, effective debt collection not only safeguards financial health but also reinforces the principles of responsible borrowing and lending.

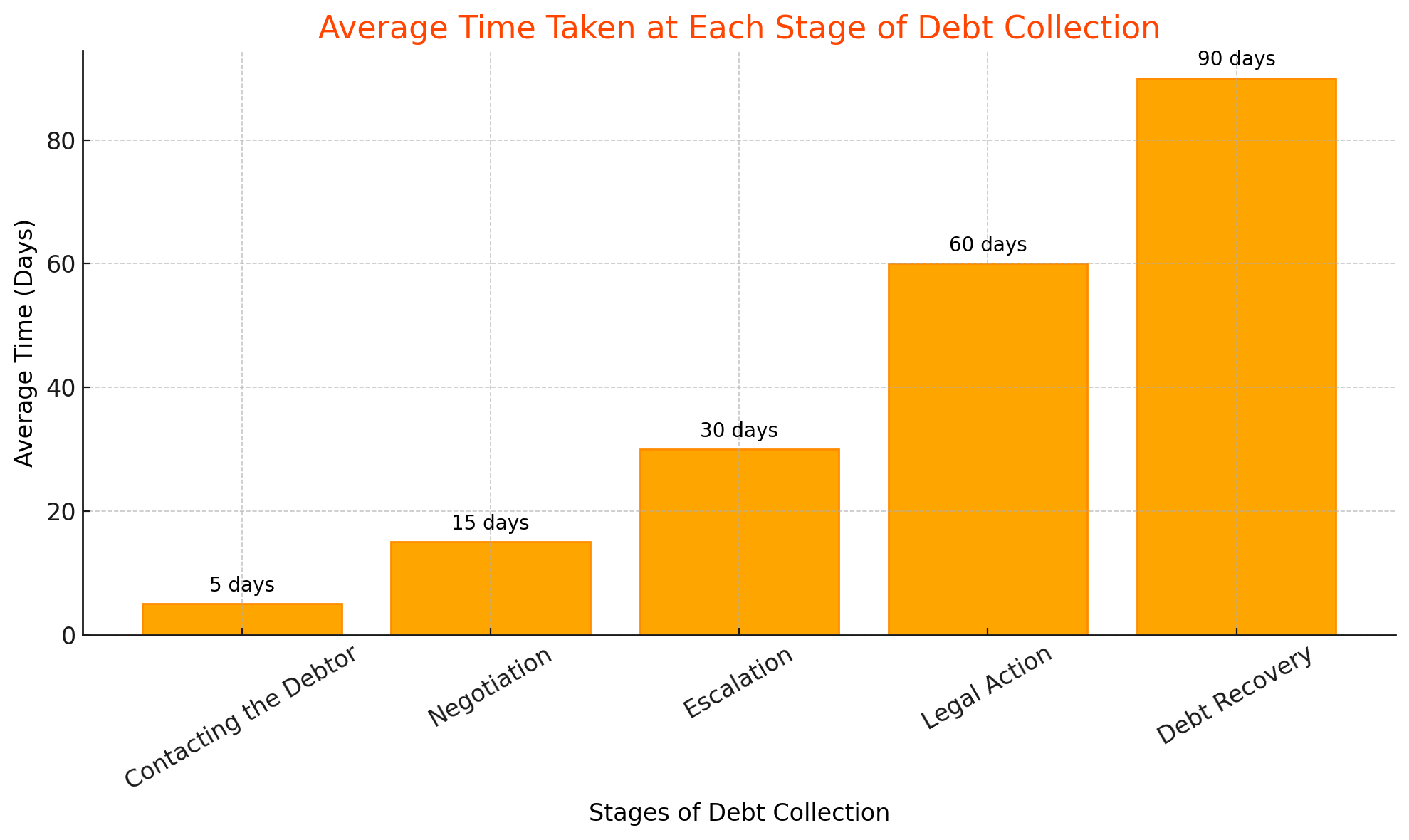

Stages of the Debt Collection Process

The debt collection process is a structured approach designed to recover unpaid debts while providing borrowers opportunities to address their financial obligations. Below are the key stages involved:

1. Initial Delinquency

This stage begins when a borrower misses one or two payments.

- Missed Payments: Borrowers are notified about their overdue payments.

- Communication: Lenders typically send reminders via phone, email, or written notices to inform borrowers of the situation.

- Temporary Arrangements: Borrowers may be offered options like temporary payment breaks or reduced payments to help them get back on track.

2. Escalated Contact

After three or four missed payments, creditors intensify their efforts.

- Firm Communication: The tone of reminders becomes stronger, emphasizing the urgency of resolving the debt.

- Default Notice: In jurisdictions like the UK, creditors may issue a default notice under the Consumer Credit Act, signaling serious consequences for non-payment.

- Referral to Debt Advice Agencies: Borrowers are often directed to agencies that can provide free or low-cost debt counseling.

3. Legal and Advanced Recovery Actions

If payments remain outstanding after multiple missed deadlines, creditors may take more aggressive steps.

- Referral to Collection Agencies: Debts are often handed over to specialized agencies for recovery.

- Court Actions: Legal proceedings, such as judgments or wage garnishments, may be initiated to recover the owed amount.

- Credit Report Impact: Unresolved debts can negatively affect credit reports, potentially hindering future access to loans or financial services.

Each stage in the debt collection process balances the need for recovery with providing borrowers opportunities to address their obligations. Understanding these steps helps both lenders and borrowers navigate the process more effectively.

Your Rights and Protections in Debt Collection

Understanding your rights during the debt collection process is vital to ensuring fair treatment and avoiding undue stress. Legal frameworks like the Fair Debt Collection Practices Act (FDCPA) provide comprehensive protections for consumers.

Key Consumer Protections Under the FDCPA

- Restrictions on Contact Methods and Timing: Debt collectors are prohibited from contacting you at inconvenient times, such as before 8 a.m. or after 9 p.m. They cannot reach out to you at work if you’ve explicitly informed them that personal calls are not allowed there.

- Prohibition of Harassment and Deceptive Practices: Collectors cannot harass, threaten, or use abusive language during communication. Misrepresentation, such as pretending to be a government agency or making false claims about legal consequences, is strictly forbidden.

- Rights to Dispute and Validate Debts: You have the right to request a debt validation letter within five days of first contact. This letter must include:

- The amount of the debt.

- The name of the original creditor.

- Your right to dispute the debt within 30 days.

- Privacy Protections: Collectors cannot disclose your debt to third parties, such as neighbors or employers. Social media contact is allowed only through private messages, and only if you have not requested otherwise.

Practical Steps for Dealing with Collectors

- Request a Validation Letter: Always confirm the debt is legitimate before making any payments. Ensure the details, including the amount and creditor, are accurate.

- Negotiate Repayment Terms: Depending on your financial situation, you may be able to negotiate a lump sum settlement or set up a manageable repayment plan. Ensure any agreements are provided in writing to avoid misunderstandings.

- Keep Detailed Records: Document all interactions with debt collectors, including dates, times, and the content of discussions. Save any letters or notices for your records.

Understanding your rights empowers you to navigate the debt collection process with confidence and ensures fair treatment by debt collectors. By leveraging these protections, you can take control of your financial obligations and work toward resolution without unnecessary stress.

Challenges in the Debt Collection Process

The debt collection process poses unique challenges for both creditors and debtors, requiring careful navigation to ensure fairness, legal compliance, and effective resolution.

For Creditors

- Balancing Legal Compliance and Recovery Goals: Adhering to strict regulations like the Fair Debt Collection Practices Act (FDCPA) while maintaining efficiency in recovering delinquent accounts. Avoiding actions that could lead to penalties or legal disputes due to non-compliance.

- Managing Multi-Jurisdictional Accounts: Handling accounts across regions with differing legal frameworks and consumer protection laws. Adjusting collection strategies to align with local regulations and practices.

- Preserving Customer Relationships: Implementing collection methods that minimize damage to the lender-borrower relationship. Maintaining professionalism and empathy to retain goodwill and avoid reputational harm.

For Debtors

- Understanding Complex Repayment Terms: Navigating repayment plans or settlements that may involve legal jargon or unclear terms. Ensuring that agreements align with their financial capacity without exacerbating the debt burden.

- Avoiding Scams and Predatory Practices: Identifying legitimate debt collectors amidst a rise in fraudulent schemes. Exercising caution with collectors who may use deceptive or harassing practices to force payments.

- Managing Financial and Emotional Stress: Coping with the pressure of persistent collection efforts while maintaining day-to-day financial stability. Addressing the impact of debt collection on mental health and creditworthiness.

Navigating the Challenges

Both creditors and debtors must adopt informed strategies to overcome these challenges. Creditors can prioritize compliance and customer engagement, while debtors can educate themselves on their rights and seek assistance from trusted financial advisors or legal professionals.

By addressing these issues proactively, the debt collection process can become less adversarial and more effective for all parties involved.

For a deeper dive into overcoming these challenges, explore our complete guide on how to recover unpaid invoices from businesses.

Practical Strategies for Managing Debt Collection

Effectively navigating the debt collection process requires proactive strategies tailored to the needs and responsibilities of both lenders and borrowers. By adopting these practices, both parties can minimize conflicts and achieve more favorable outcomes.

For Lenders

- Using Clear and Concise Language in Agreements: Ensure loan agreements and repayment terms are written in plain, understandable language. Avoid jargon to reduce the risk of misunderstandings that can lead to disputes.

- Offering Flexible Repayment Options: Provide options like payment plans, temporary deferrals, or reduced payment schedules to help borrowers avoid defaults. Tailor solutions to individual financial situations while protecting the lender’s interests.

- Investing in Robust Collection Strategies: Implement systematic approaches to debt collection, such as automated reminders and detailed tracking of accounts. Train collection teams to handle interactions professionally, adhering to legal guidelines and maintaining customer relationships.

For Borrowers

- Understanding the Terms of Debt Collection Agreements: Review agreements thoroughly to know your rights and obligations during the collection process. Seek clarification from lenders on unclear terms before signing.

- Seeking Debt Counseling or Professional Advice Early: Engage with credit counselors or financial advisors at the first sign of financial strain. Leverage their expertise to explore repayment options or negotiate with creditors effectively.

- Keeping Communication Lines Open with Creditors: Proactively inform creditors of any financial difficulties to explore alternative payment arrangements. Respond promptly to creditor communications to avoid escalation and maintain trust.

By prioritizing communication, flexibility, and professionalism, lenders and borrowers can work together to address financial challenges. This approach not only ensures better compliance with legal frameworks but also fosters long-term financial stability and trust between both parties.

Navigating the Debt Collection Process

Scenario: A Small Business Owner Falls Behind on Credit Card Payments

A small business owner, overwhelmed by financial challenges due to declining sales, finds it difficult to meet monthly credit card payments. Here’s how the debt collection process unfolded and how they managed to resolve it.

Stage 1: Initial Delinquency

What Happened:

The business owner missed two consecutive monthly payments. The creditor started sending reminders through phone calls and emails, encouraging them to bring their account up to date.

Actions Taken:

To avoid further escalation, the owner reached out to the creditor and negotiated a temporary payment plan that reduced monthly payments for a short period.

Impact:

- Missed payments were reported to credit bureaus, slightly lowering the credit score.

- The temporary arrangement provided some breathing room to manage finances.

Stage 2: Default Notice and Transfer to a Debt Collection Agency

What Happened:

After missing additional payments, the creditor issued a default notice as required under consumer credit regulations. The account was then sold to a debt collection agency for recovery.

Actions Taken:

The owner received a debt validation letter from the agency and confirmed the debt’s legitimacy. They avoided ignoring calls and instead engaged in discussions with the agency to explore options.

Impact:

- The debt being managed by a collection agency created additional stress.

- Communication with the agency prevented further penalties and established trust for negotiations.

Stage 3: Legal Action by Creditors

What Happened:

The agency warned of legal action due to continued non-payment. A court judgment was sought, which could result in wage garnishment or a lien on the business’s assets.

Actions Taken:

Before the court date, the owner negotiated a structured repayment plan with the agency, avoiding legal proceedings. They prioritized payments to rebuild their credit score and stabilize their finances.

Impact:

- Legal action was averted, preventing additional damage to the credit score.

- The repayment plan allowed the owner to regain control over their financial obligations.

Resolution and Recovery

Outcome:

The structured repayment plan helped the business owner gradually pay off the debt. With consistent payments, their credit score began to recover, and they could refocus on growing the business.

Key Takeaways:

- Early communication with creditors is crucial to avoid escalation.

- Understanding rights under debt collection laws ensures fair treatment.

- A proactive approach to repayment can prevent long-term financial damage.

Steps to Avoid Debt Collection Issues

Avoiding debt collection begins with proactive financial management and a solid understanding of your financial responsibilities. By taking preventive measures and staying informed, both creditors and borrowers can reduce the likelihood of delinquency and maintain healthy financial relationships.

Proactive Financial Management Tips

- Set Up Automatic Payments: Automate bill payments to ensure deadlines are consistently met, minimizing the risk of late fees or missed payments. Use a dedicated account for recurring transactions to simplify tracking.

- Monitor Credit Reports Regularly: Regularly review credit reports to identify errors or unresolved debts. Address discrepancies early to maintain a strong credit score.

The Role of Education in Preventing Delinquency

- Understanding Contractual Obligations: Fully grasp the terms of repayment, interest rates, and penalties outlined in agreements. Consult financial experts for clarification if terms are unclear.

- Building Financial Literacy: Develop budgeting skills to prioritize expenses and manage debts effectively. Take advantage of financial education resources, such as workshops or online courses, to strengthen your financial decision-making abilities.

Conclusion

Understanding the debt collection process is essential for maintaining financial stability and fostering trust between creditors and debtors.

Don’t leave your legal matters to chance. Our team of legal experts specializes in providing clear, actionable guidance for navigating debt collection challenges. Contact us today to secure your rights and protect your interests with expert legal support!